How much does a ticket to the Met Gala cost?

Met Gala ticket prices cost far more in 2024 than they did last year. How much is a ticket?

Watch CBS News

Met Gala ticket prices cost far more in 2024 than they did last year. How much is a ticket?

Steward Health Care, the struggling hospital group that owns hospitals in Massachusetts, Texas, Florida and other states, announced Monday that it is filing for bankruptcy.

Hormel Foods says potentially contaminated products were shipped to Publix and Dollar Tree distribution warehouses.

The IRS is tapping Inflation Reduction Act funding to hire more agents and go after more tax cheats. Here's where it is focusing.

Warren Buffett referred to close friend Charlie Munger as the "the architect of Berkshire Hathaway."

A Georgia senior living community fired an elderly worker shortly after honoring her as an employee of the year, regulators allege.

U.S. unemployment rate rose slightly to 3.9% in April, continuing a stretch of remaining under 4% for 27 months.

Audit firm BF Borgers allegedly failed to comply with accounting standards and fabricated audit documentation, regulators claim.

Condé Nast employees were set to walk off the job only hours before the Met Gala, chaired by company editorial director Anna Wintour.

Want to take advantage of what debt forgiveness offers? Here's what to avoid if you're trying to take this route.

Are you wondering what you should do with your savings ahead of the next inflation report? Find out here.

Considering accessing your home equity this month? Then you'll want to make these three strategic moves.

Tesla accounted for 80% of electric vehicle sales in the U.S. in 2020, but that figure fell to 55% last year.

The generative artificial intelligence boom has led to the emergence of romantic companion bots.

Apple said it will stop selling the devices later this month in order to comply with a U.S. import ban.

Alex Jones, the conspiracy theorist known for his fake news site InfoWars and his false denial of the Sandy Hook massacre, was permanently banned from Twitter in 2018.

More than 90 million consumers will scan a QR code this year. But the technology can also facilitate identity theft.

The billionaire owner of X took a defensive tone, saying that "the whole world will know that those advertisers killed the company."

OpenAI co-founder Sam Altman says he's looking forward to returning to the company, with the support of Microsoft's CEO, to build the 2 companies' "strong partnership."

Musk, who is under fire for supporting an antisemitic post, said the money will be donated to hospitals in Israel and to the Red Cross in Gaza.

Altman landed at Microsoft, the biggest investor in OpenAI, as former Twitch leader Emmett Shear was named OpenAI's new chief executive.

Prosecutors are continuing to call witnesses in former President Donald Trump's criminal trial in New York, where jurors heard from a former Trump Organization executive.

A U.S. soldier has been detained in Russia, National Security Council spokesman John Kirby confirmed.

Israel has not yet officially commented on Hamas' response to the reported ceasefire proposal.

South Dakota Gov. Kristi Noem would not answer a question about whether the meeting with the North Korean leader actually occurred.

Two astronauts will put the Boeing Starliner through its paces to verify it's ready to begin launching operational crew ferry flights to the space station.

Police identified the victims as Samantha Cisneros and Taryn Allen and said a 5-year-old girl was injured with a gunshot wound.

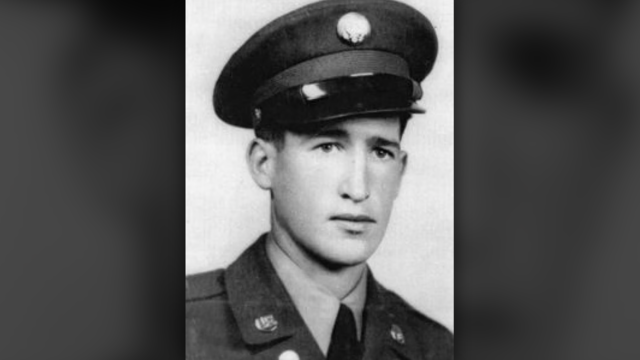

A 19-year-old U.S. soldier from Colorado has been accounted for more than 70 years after being declared missing in action in the Korean War.

A man was also found shot to death inside the home where the man who pulled the gun during the service.

Miss USA Noelia Voigt said she's stepping down and relinquishing her crown.

With a relatively low average monthly cost of living and a low crime rate, this little-known town has a lot to offer retirees according to one report.

The U.S. is reaching "peak 65," marking the largest retirement wave in American history. But the financial outlook for many is grim.

Americans are underprepared for retirement, with the average account holding just $88,400 in savings.

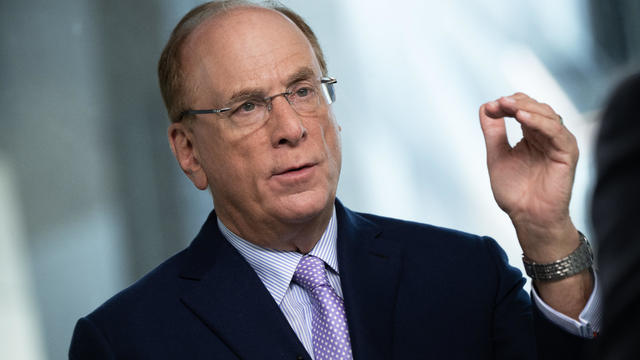

BlackRock CEO Larry Fink said that longer life expectancies are "putting the U.S. retirement system under immense strain."

About 1 in 8 workers think they'll retire by age 61. But the reality of saving for decades of expenses is daunting.

A 19-year-old U.S. soldier from Colorado has been accounted for more than 70 years after being declared missing in action in the Korean War.

Prosecutors are continuing to call witnesses in former President Donald Trump's criminal trial in New York, where jurors heard from a former Trump Organization executive.

Miss USA Noelia Voigt said she's stepping down and relinquishing her crown.

Two astronauts will put the Boeing Starliner through its paces to verify it's ready to begin launching operational crew ferry flights to the space station.

South Dakota Gov. Kristi Noem would not answer a question about whether the meeting with the North Korean leader actually occurred.

Condé Nast employees were set to walk off the job only hours before the Met Gala, chaired by company editorial director Anna Wintour.

Hormel Foods says potentially contaminated products were shipped to Publix and Dollar Tree distribution warehouses.

Met Gala ticket prices cost far more in 2024 than they did last year. How much is a ticket?

Steward Health Care, the struggling hospital group that owns hospitals in Massachusetts, Texas, Florida and other states, announced Monday that it is filing for bankruptcy.

Warren Buffett referred to close friend Charlie Munger as the "the architect of Berkshire Hathaway."

Prosecutors are continuing to call witnesses in former President Donald Trump's criminal trial in New York, where jurors heard from a former Trump Organization executive.

A U.S. soldier has been detained in Russia, officials confirmed.

Israel has not yet officially commented on Hamas' response to the reported ceasefire proposal.

South Dakota Gov. Kristi Noem would not answer a question about whether the meeting with the North Korean leader actually occurred.

The 82-year-old senator from Vermont announced in a video posted on social media that he will seek a fourth term in the Senate.

A survey from the American Academy of Dermatology finds more than one-third of adults reported getting a sunburn last year — the highest number since 2020.

Hormel Foods says potentially contaminated products were shipped to Publix and Dollar Tree distribution warehouses.

Steward Health Care, the struggling hospital group that owns hospitals in Massachusetts, Texas, Florida and other states, announced Monday that it is filing for bankruptcy.

The Texas dairy worker infected by H5N1 "did not disclose the name of their workplace," frustrating investigators.

Stress is hard to avoid, but experts say getting outdoors can have a positive impact on both our mental and physical health.

A U.S. soldier has been detained in Russia, officials confirmed.

Israel has not yet officially commented on Hamas' response to the reported ceasefire proposal.

Zakia Wardak, Afghanistan's top diplomat in India, announced her resignation after reportedly being stopped at an airport with the gold cache.

Claiming a "new round of escalation" from NATO amid the war in Ukraine, Russia plans drills simulating the use of battlefield nuclear weapons.

Historic flooding has left the wealthy Brazilian city of Porto Alegre underwater, with more than 80 people dead and many awaiting rescue.

Miss USA Noelia Voigt said she's stepping down and relinquishing her crown.

Kendrick Lamar and Drake have each released several ruthless diss tracks against each other, with Kendrick alleging Drake has a secret daughter and making other disturbing accusations.

Cedric the Entertainer gives an exclusive first look at tonight's season six finale of "The Neighborhood."

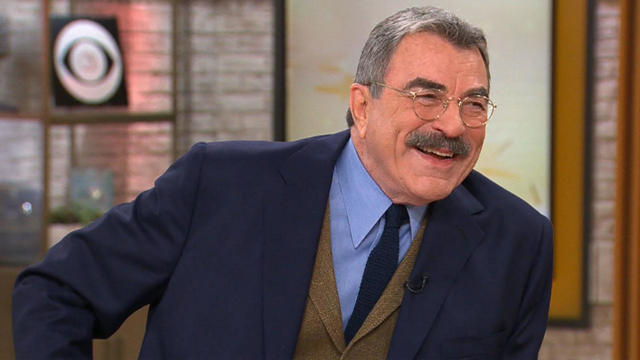

From "Magnum, P.I." to "Blue Bloods," Tom Selleck has become a staple of American television and film. In his latest memoir, "You Never Know," Selleck shares insights from his journey in Hollywood and beyond.

It's widely known the Met Gala itself includes a dinner and a performance. But aside from bathroom selfies and elevator clips, the gala itself isn't recorded.

Sidechat, an app launched in 2022 where students can post anonymously about their colleges, is becoming a tool for those choosing to protest at U.S. campuses. Amanda Silberling, a senior culture writer for TechCrunch, joins CBS News with more details on the app.

Microsoft users can now use biometric passkeys, like a thumbprint or Face ID, to sign into Microsoft 365, Copilot. Jon Fingas, senior editor at Techopedia, has more.

From labor shortages to environmental impacts, farmers are looking to AI to help revolutionize the agriculture industry. One California startup, Farm-ng, is tapping into the power of AI and robotics to perform a wide range of tasks, including seeding, weeding and harvesting.

Sidechat, an anonymous messaging app, has been used by students to share opinions and updates, but university administrators say it has also fueled hateful rhetoric.

Georgia is home to the nation's newest nuclear reactor. It's bringing clean energy to the state, but the project has run over budget and past its original completion date. Drew Kann, climate and environment reporter for The Atlanta Journal-Constitution, joins CBS News to explore the effort.

Reported sightings of giant, toxic, invasive hammerhead flatworms are on the rise in parts of southeastern Canada. Experts say the worms can grow up to 3 feet long and pose a risk to children, pets and other small animals. Peter Ducey, PH.D. and distinguished teaching professor at SUNY Cortland, joins CBS News to discuss the worm.

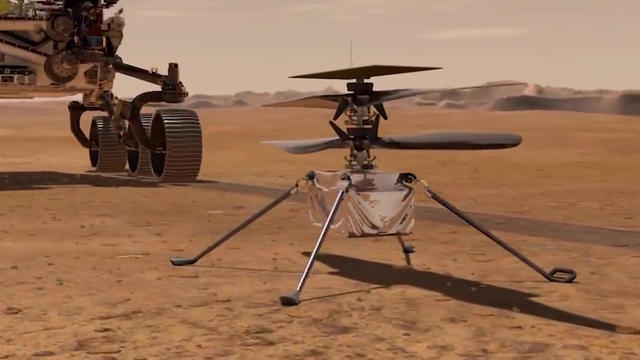

When NASA added a tiny four-pound helicopter as a stowaway to its Mars 2020 lander, it expected the helicopter to fly five very brief flights in the thin Martian atmosphere. Yet, Ingenuity would far surpass all expectations.

When NASA added a drone named Ingenuity to its Mars 2020 rover Perseverance, it expected the tiny four-pound helicopter to fly a total of five very brief missions in the thin Martian atmosphere. But Ingenuity far surpassed all expectations, flying dozens of flights before suffering damage to its rotors in January. Correspondent David Pogue reports on how the tiny drone, created from off-the-shelf parts, continued to provide valuable data and images from the Red Planet three years into its mission.

There's a newly-determined "major factor" in declining bumblebee populations – and it's attacking their nests.

On Monday, Boeing plans to launch astronauts on its new spacecraft that is called Starliner. The test flight to the International Space Station is years behind schedule.

A man has confessed to killing a woman at her apartment near Oklahoma City in 2016. He is being held on a first-degree murder charge.

Police identified the victims as Samantha Cisneros and Taryn Allen and said a 5-year-old girl was injured with a gunshot wound.

A church service in North Braddock, Pennsylvania, was upended Sunday when a man pulled a gun on the pastor in the middle of his sermon.

Officials confirmed the bodies found in a well last week in Mexico belonged to three missing surfers and that they each had bullet wounds.

Brian Fanion says he and his wife Amy Fanion had been arguing about his retirement plans when she picked up his service weapon and shot herself. Investigators did not believe his story.

Two astronauts will put the Boeing Starliner through its paces to verify it's ready to begin launching operational crew ferry flights to the space station.

After years of delays, Boeing is set to launch its Starliner spacecraft with a crew for the first time Monday. The test flight will carry two astronauts to the International Space Station.

The Eta Aquariids meteor shower will peak overnight on Sunday into Monday, according to NASA.

Two veteran astronauts will put the Starliner through its paces in the ship's first piloted flight to orbit.

Boeing is expected to launch its Starliner space capsule that will take two astronauts to the International Space Station. CBS News consultant Bill Harwood breaks down Boeing's mission.

A look back at the esteemed personalities who've left us this year, who'd touched us with their innovation, creativity and humanity.

The Francis Scott Key Bridge in Baltimore collapsed early Tuesday, March 26 after a column was struck by a container ship that reportedly lost power, sending vehicles and people into the Patapsco River.

When Tiffiney Crawford was found dead inside her van, authorities believed she might have taken her own life. But could she shoot herself twice in the head with her non-dominant hand?

We look back at the life and career of the longtime host of "Sunday Morning," and "one of the most enduring and most endearing" people in broadcasting.

Cayley Mandadi's mother and stepfather go to extreme lengths to prove her death was no accident.

Saving for retirement is a big concern for many Americans, even those who are considered high-earners. But sometimes, if your income is considered too high, you might miss out on some great savings options. That's where something called a backdoor Roth IRA comes in. CBS News business analyst Jill Schlesinger has more.

Columbia University announced Monday it will be canceling its main commencement ceremony amid protests over the Israel-Hamas war. Columbia is the latest school forced to change their plans following a wave of protests. CBS News correspondent Lana Zak is at Columbia with more.

Some commentators have compared the campus protests over the war in Gaza to the anti-Vietnam war movement and other past protests. CBS News' Anne-Marie Green looks back at how some past students made their voices heard.

The federal judge in Donald Trump's New York criminal case has found the former president in contempt again for violating his gag order and is now threatening him with jail time for his continued behavior. Attorney and CBS News campaign reporter Katrina Kaufman and CBS News investigative reporter Graham Kates have more.

Chinese President Xi Jinping is meeting with French President Emmanuel Macron in Paris Monday as part of a multi-day trip across Europe, his first since the pandemic. It's expected they'll discuss efforts to end Russia's war in Ukraine. CBS News foreign correspondent Elaine Cobbe has more.