Some students want their colleges to divest from Israel. Here's what that really means.

College protesters are demanding divestment as a way to deliver change, although its effectiveness isn't clear cut.

Watch CBS News

College protesters are demanding divestment as a way to deliver change, although its effectiveness isn't clear cut.

Without a major change, Social Security may be forced to cut benefits in 2035, a year later than previously forecast.

A new membership from luxury fitness chain Equinox includes a battery of tests normally reserved for professional athletes.

Met Gala ticket prices cost far more in 2024 than they did last year. How much is a ticket?

Hormel Foods says potentially contaminated products were shipped to Publix and Dollar Tree distribution warehouses.

Steward Health Care, the struggling hospital group that owns hospitals in Massachusetts, Texas, Florida and other states, announced Monday that it is filing for bankruptcy.

Recall includes yogurt pretzels and other confections sold by retailers such as Dollar General, HyVee, Target and Walmart.

The IRS is tapping Inflation Reduction Act funding to hire more agents and go after more tax cheats. Here's where it is focusing.

Condé Nast employees were set to walk off the job only hours before the Met Gala, chaired by company editorial director Anna Wintour.

Are you a beginner investor considering buying gold? Here are three times you should and two times you shouldn't.

Want to take advantage of what debt forgiveness offers? Here's what to avoid if you're trying to take this route.

Are you wondering what you should do with your savings ahead of the next inflation report? Find out here.

Tesla accounted for 80% of electric vehicle sales in the U.S. in 2020, but that figure fell to 55% last year.

The generative artificial intelligence boom has led to the emergence of romantic companion bots.

Apple said it will stop selling the devices later this month in order to comply with a U.S. import ban.

Alex Jones, the conspiracy theorist known for his fake news site InfoWars and his false denial of the Sandy Hook massacre, was permanently banned from Twitter in 2018.

More than 90 million consumers will scan a QR code this year. But the technology can also facilitate identity theft.

The billionaire owner of X took a defensive tone, saying that "the whole world will know that those advertisers killed the company."

OpenAI co-founder Sam Altman says he's looking forward to returning to the company, with the support of Microsoft's CEO, to build the 2 companies' "strong partnership."

Musk, who is under fire for supporting an antisemitic post, said the money will be donated to hospitals in Israel and to the Red Cross in Gaza.

Altman landed at Microsoft, the biggest investor in OpenAI, as former Twitch leader Emmett Shear was named OpenAI's new chief executive.

Stormy Daniels is in New York and expects to be called to the stand to testify Tuesday, according to two sources familiar with the matter.

An Israeli tank unit has rolled in to take "operational control" of the Gaza side of the crucial Rafah border crossing amid talks for a truce.

The Supreme Court is set to issue decisions in the coming weeks in more than a dozen cases involving issues like abortion, guns and sweeping immunity for former President Donald Trump.

South African rescuers are "actually hearing people through the rubble" after a building collapsed in the city of George.

Without a major change, Social Security may be forced to cut benefits in 2035, a year later than previously forecast.

A Moscow court says a U.S. man has been jailed for drunkenly crashing through a kid's library window, as an American soldier is also detained.

A tornado destroyed homes and toppled trees and power lines when it roared through a small northeast Oklahoma city, one of several twisters that erupted in the central United States amid a series of powerful storms.

A Kansas City-area man, 75, admitted he killed his hospitalized wife, saying he couldn't take care of her or afford her medical bills, court records say.

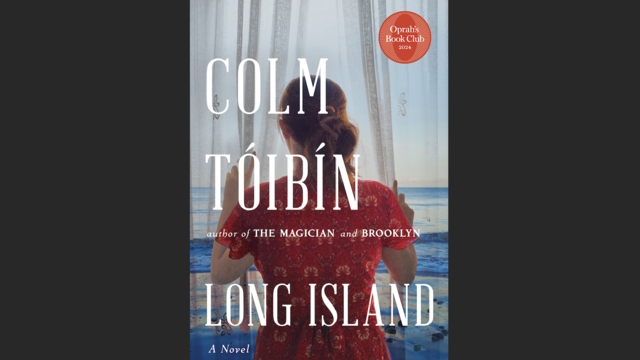

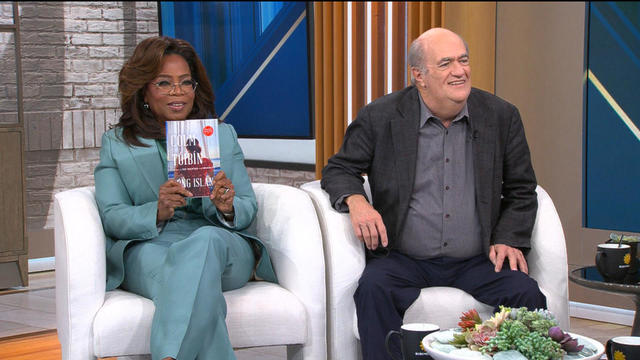

Oprah Winfrey has selected "Long Island" by author Colm Tóibín as her newest book club pick.

With a relatively low average monthly cost of living and a low crime rate, this little-known town has a lot to offer retirees according to one report.

The U.S. is reaching "peak 65," marking the largest retirement wave in American history. But the financial outlook for many is grim.

Americans are underprepared for retirement, with the average account holding just $88,400 in savings.

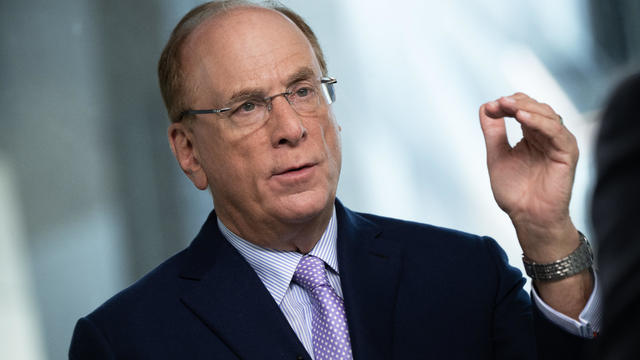

BlackRock CEO Larry Fink said that longer life expectancies are "putting the U.S. retirement system under immense strain."

About 1 in 8 workers think they'll retire by age 61. But the reality of saving for decades of expenses is daunting.

The Supreme Court is set to issue decisions in the coming weeks in more than a dozen cases involving issues like abortion, guns and sweeping immunity for former President Donald Trump.

Stormy Daniels is in New York and expects to be called to the stand to testify Tuesday, according to two sources familiar with the matter.

The visualization, produced on a NASA supercomputer, allows users to experience flight towards a supermassive black hole.

A Kansas City-area man, 75, admitted he killed his hospitalized wife, saying he couldn't take care of her or afford her medical bills, court records say.

A tornado destroyed homes and toppled trees and power lines when it roared through a small northeast Oklahoma city, one of several twisters that erupted in the central United States amid a series of powerful storms.

Heineken said the investment is a demonstration of "confidence in the resilience of the great British local in the face of uncertainty."

Recall includes yogurt pretzels and other confections sold by retailers such as Dollar General, HyVee, Target and Walmart.

Without a major change, Social Security may be forced to cut benefits in 2035, a year later than previously forecast.

College protesters are demanding divestment as a way to deliver change, although its effectiveness isn't clear cut.

A new membership from luxury fitness chain Equinox includes a battery of tests normally reserved for professional athletes.

The Supreme Court is set to issue decisions in the coming weeks in more than a dozen cases involving issues like abortion, guns and sweeping immunity for former President Donald Trump.

Stormy Daniels is in New York and expects to be called to the stand to testify Tuesday, according to two sources familiar with the matter.

Prosecutors are continuing to call witnesses in former President Donald Trump's criminal trial in New York, where jurors heard from a former Trump Organization executive.

Without a major change, Social Security may be forced to cut benefits in 2035, a year later than previously forecast.

A U.S. soldier has been detained in Russia, officials confirmed.

Recall includes yogurt pretzels and other confections sold by retailers such as Dollar General, HyVee, Target and Walmart.

A survey from the American Academy of Dermatology finds more than one-third of adults reported getting a sunburn last year — the highest number since 2020.

Hormel Foods says potentially contaminated products were shipped to Publix and Dollar Tree distribution warehouses.

Steward Health Care, the struggling hospital group that owns hospitals in Massachusetts, Texas, Florida and other states, announced Monday that it is filing for bankruptcy.

The Texas dairy worker infected by H5N1 "did not disclose the name of their workplace," frustrating investigators.

South African rescuers are "actually hearing people through the rubble" after a building collapsed in the city of George.

Erin Patterson, who is accused of serving her ex-husband's family death cap mushrooms with lunch, pleaded not guilty to eight charges of murder and attempted murder.

Heineken said the investment is a demonstration of "confidence in the resilience of the great British local in the face of uncertainty."

Ukraine's national weightlifting coach said Oleksandr Pielieshenko "died a hero defending" his country from Russian forces.

A Moscow court says a U.S. man has been jailed for drunkenly crashing through a kid's library window, as an American soldier is also detained.

Gayle King gives viewers a behind-the-scenes look at her preparation and journey to the Met Gala.

Oprah Winfrey unveils "Long Island" as her latest book club pick on "CBS Mornings." The sequel to Colm Tóibín's best-selling novel "Brooklyn," "Long Island" continues the story of Eilis Lacey more than two decades later now as a mother and wife in America.

The 2024 Met Gala saw hundreds of celebrities looking their best on fashion's biggest night.

The stars came out for the the 2024 Met Gala in New York City. See some of the most eye-catching outfits of the night.

Miss USA Noelia Voigt said she's stepping down and relinquishing her crown.

Boeing's Starliner was set to make its maiden voyage to the International Space Station, with its first piloted launch Monday night. But the launch, already pushed back following years of delays, was scrubbed with less than two hours to go before liftoff. Mark Strassmanm reports.

Sidechat, an app launched in 2022 where students can post anonymously about their colleges, is becoming a tool for those choosing to protest at U.S. campuses. Amanda Silberling, a senior culture writer for TechCrunch, joins CBS News with more details on the app.

From labor shortages to environmental impacts, farmers are looking to AI to help revolutionize the agriculture industry. One California startup, Farm-ng, is tapping into the power of AI and robotics to perform a wide range of tasks, including seeding, weeding and harvesting.

Microsoft users can now use biometric passkeys, like a thumbprint or Face ID, to sign into Microsoft 365, Copilot. Jon Fingas, senior editor at Techopedia, has more.

Sidechat, an anonymous messaging app, has been used by students to share opinions and updates, but university administrators say it has also fueled hateful rhetoric.

Boeing's Starliner was set to make its maiden voyage to the International Space Station, with its first piloted launch Monday night. But the launch, already pushed back following years of delays, was scrubbed with less than two hours to go before liftoff. Mark Strassmanm reports.

Reported sightings of giant, toxic, invasive hammerhead flatworms are on the rise in parts of southeastern Canada. Experts say the worms can grow up to 3 feet long and pose a risk to children, pets and other small animals. Peter Ducey, PH.D. and distinguished teaching professor at SUNY Cortland, joins CBS News to discuss the worm.

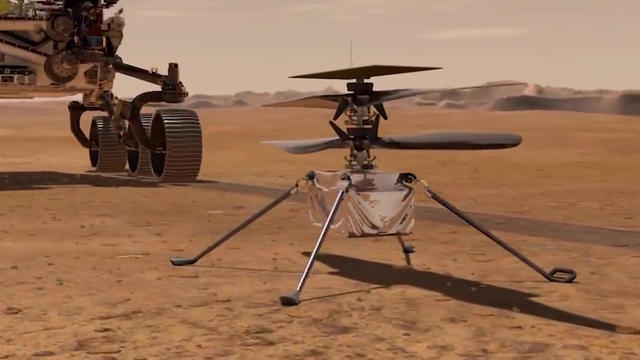

When NASA added a tiny four-pound helicopter as a stowaway to its Mars 2020 lander, it expected the helicopter to fly five very brief flights in the thin Martian atmosphere. Yet, Ingenuity would far surpass all expectations.

When NASA added a drone named Ingenuity to its Mars 2020 rover Perseverance, it expected the tiny four-pound helicopter to fly a total of five very brief missions in the thin Martian atmosphere. But Ingenuity far surpassed all expectations, flying dozens of flights before suffering damage to its rotors in January. Correspondent David Pogue reports on how the tiny drone, created from off-the-shelf parts, continued to provide valuable data and images from the Red Planet three years into its mission.

There's a newly-determined "major factor" in declining bumblebee populations – and it's attacking their nests.

Erin Patterson, who is accused of serving her ex-husband's family death cap mushrooms with lunch, pleaded not guilty to eight charges of murder and attempted murder.

A Kansas City-area man, 75, admitted he killed his hospitalized wife, saying he couldn't take care of her or afford her medical bills, court records say.

Jake and Callum Robinson from Australia and American Jack Carter Rhoad were shot in the head, their bodies dumped in a covered well miles away.

A man has confessed to killing a woman at her apartment near Oklahoma City in 2016. He is being held on a first-degree murder charge.

Police identified the victims as Samantha Cisneros and Taryn Allen and said a 5-year-old girl was injured with a gunshot wound.

The visualization, produced on a NASA supercomputer, allows users to experience flight towards a supermassive black hole.

Boeing's Starliner space capsule is set for a historic launch Monday night. CBS News space consultant Bill Harwood looks at the long-awaited mission into orbit, and what it could mean for the future of space travel.

Boeing's Starliner was set to make its maiden voyage to the International Space Station, with its first piloted launch Monday night. But the launch, already pushed back following years of delays, was scrubbed with less than two hours to go before liftoff. Mark Strassmanm reports.

The planned piloted launch of Boeing's long-delayed Starliner crew ferry ship was called off with less than two hours to go before liftoff.

After years of delays, Boeing is set to launch its Starliner spacecraft with a crew for the first time Monday. The test flight will carry two astronauts to the International Space Station.

A look back at the esteemed personalities who've left us this year, who'd touched us with their innovation, creativity and humanity.

The Francis Scott Key Bridge in Baltimore collapsed early Tuesday, March 26 after a column was struck by a container ship that reportedly lost power, sending vehicles and people into the Patapsco River.

When Tiffiney Crawford was found dead inside her van, authorities believed she might have taken her own life. But could she shoot herself twice in the head with her non-dominant hand?

We look back at the life and career of the longtime host of "Sunday Morning," and "one of the most enduring and most endearing" people in broadcasting.

Cayley Mandadi's mother and stepfather go to extreme lengths to prove her death was no accident.

There is new research from the journal Environmental Science and Technology that is raising concerns about toxic chemicals coming from the seats inside of cars. Most seats are treated with flame-retardant chemicals because of a federal fire safety standard. The new study found those chemicals in the air inside of cars, which means drivers or passengers could be inhaling them.

Stormy Daniels expects to be called to testify in Donald Trump's New York criminal trial on Tuesday, sources say. The adult film star received a "hush money" payment in 2016 to buy her silence about an alleged sexual encounter with Trump. Attorney and CBS News campaign reporter Katrina Kaufman has more.

Gayle King gives viewers a behind-the-scenes look at her preparation and journey to the Met Gala.

The Israeli military has taken control of the Palestinian side of the Rafah crossing on Egypt's border after the Netanyahu government rejected an Egyptian-Qatari mediated cease-fire proposal that was approved by Hamas, which included the release of hostages.

Israel claims to have seized control of the Gaza side of the Rafah border crossing with Egypt as its military appears to push ahead with an offensive in Rafah. Despite the development, mediators are still scrambling to negotiate a cease-fire deal between Israel and Hamas. CBS News foreign correspondent Ramy Inocencio has more.